Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Broker’s Perspective: Seattle Market Slows, Stanwood-Camano Area Market Holds Its Own

Windermere Stanwood-Camano brokers are deeply connected to the issues that face local home-buyers and sellers. In this series of blogs, The Broker’s Perspective, Windermere Stanwood-Camano brokers provide insight into current market trends and topics. Below is an excerpt from an article by Seattle Times columnist, Jon Talton, followed by a Q&A with Managing Broker of Camano Country Club, Beth Newton.

Slowing real estate might let us catch our breath — or knock the wind out of us

By: Jon Talton, Seattle Times Columnist

If you read my colleague Mike Rosenberg, you already know that segments of the Seattle real-estate market are slowing.

We have an apartment glut thanks to heavy investment in multifamily housing coming out of the Great Recession. Sales and inventory numbers for homes in King County are back to 2012 levels. Prices are dropping many places after record leaps in recent years.

Last week came further evidence: For the first time in about a decade, Seattle wasn’t among the top 10 markets for the coming year in the “Emerging Trends in Real Estate” report by the Urban Land Institute and PricewaterhouseCoopers. Last year, we were No. 1.

The report focuses on the Seattle-Bellevue area, setting Tacoma (No. 53) out separately. And it doesn’t directly correlate with livability. Rather, it assesses investment and development trends, and for several years has chronicled the rise of high-quality urban centers.

Many people will see this as all good news, a pause from explosive growth that has also been blamed for lower affordability, rising inequality and social ills. I would add that markets go down as well as up, and every swing creates winners and losers.

Still, while Seattle’s growth isn’t stopping, going from the equivalent of 90 miles per hour to 50 would be felt, and in some unpleasant ways, too.

“Emerging Trends” is the gold standard in real-estate forecasts, based on interviews and surveys of hundreds of leading developers, investors and lenders.

It provides a deep analysis of the outlook for residential, retail, office, hotel and industrial properties, as well as the wider economic environment.

For next year, the top overall markets according to the ULI study are Dallas-Fort Worth, Brooklyn, Raleigh-Durham, Orlando, Nashville, Austin, Boston, Denver, Charlotte and Tampa-St. Petersburg.

At No. 16, Seattle still shows a decent outlook among the 79 markets surveyed. We rank No. 20 in homebuilding prospects. And second, behind Boston, in local market attractiveness for investors. Office demand is expected to continue doing well in the central business district.

Being No. 1 isn’t everything. I’d take Seattle over almost any city among the top 10. But Seattle dropping off might mark an inflection point — emphasis on “might.”

The report also offers this caution about Seattle’s drop: “Seattle is still viewed as an attractive place in which to invest, but did media coverage of potential new supply being delivered and increased regulatory discussions sway the opinion of survey respondents?”

Hard as it is to process, Seattle also gets relatively good marks for housing affordability within the context of the Pacific Coast (Tacoma does even better). Demand remains strong for distribution space, too.

The report points to a local economy operating near capacity (e.g. employment) as a constraint on real-estate investment next year.

“This is evidenced by the comments from focus group participants in Seattle and Portland that attracting qualified labor is getting more difficult and could be hurting employment growth,” it reads.

The unemployment rate for Seattle-Tacoma-Bellevue was 3.6 percent in August.

Assuming the larger economic climate is stable, we can expect Seattle to go from “hot” to “warm.”

(article continues…)

Beth Newton, Managing Broker Camano Country Club

Beth’s Perspective

Our local market is not quite the same as the Seattle Market, how much of a change have you felt in the local Stanwood–Camano market, if any?

The local Stanwood-Camano market is definitely not the same as the Seattle market, so we have not necessarily felt any change other than the normal back to school slow-down in the September and early October market.

Some are saying that right now is the best the market has been for buyers since 2015 – do you see any indications of that holding true in the Stanwood – Camano market?

Not necessarily, though it is a dual market where the upper end high priced Real Estate prices may be coming down a little, the majority of the median priced market activity is still showing as a strong seller’s market.

The Stock market dropped, interest rates went up and Real Estate statewide seems to be slowing a little bit – do you see this as a simple market correction or a sign of something more?

This looks like a simple market correction for this time of year, or a normal flattening of the market for back to school, which is quite normal and expected. I look forward to seeing this year finishing strong. And 2019 will be the best market to come!

Choosing the Right Backsplash for Your Kitchen

Every chef’s kitchen should have a style that matches the delicious food that comes out of it. But even if you’re doing little more than making mac and cheese out of a box, your kitchen still can be a place of color and creativity. Kitchen backsplashes are nothing new, but they’ve seen a recent surge in popularity. We’re fortunate to see homes every day with creative takes on this tiling trend, so we decided to showcase some popular backsplash designs to serve as inspiration.

Glass Tile

When designing a kitchen, function and flair should work hand in hand. The appeal of glass tiling is that it’s easy to clean. Backing up the functionality is affordability. While glass tiling runs more expensive than ceramic, the cost is typically below stainless steel, and even some stones. Glass tiling is perfect for those with an artistic flair. Whether it’s simply a splash of color, a full mosaic, or even an intricate design, glass tile lets your inner artist shine. While the initial cost may be greater, glass tiling can more easily be found in pre-set sheets, making DIY installation far easier than many other types of tiles.

Ceramic Tile

If you need a backsplash that can hold up to consistent use, ceramic tile is a great fit. The most cost-effective tile to professionally install, ceramic tiling offers a glazed shine with a variety of color options. Creating a clear, simple, ceramic backsplash is a great way to add a colorful flair to your kitchen. Between the cost-effectiveness and its low-maintenance nature, ceramic is unsurprisingly the most common type of kitchen tiling.

Metallic Tile

Stainless steel is one of the more popular backsplash options for those interested in a metallic finish, but we’re also seeing more aluminum, copper, and bronze tiles. The range in metal type obviously impacts the cost, but most metal tiles are much more expensive than their ceramic counterparts – at least $10 per square foot more. For that extra cost, however, you’ll receive a sturdy backsplash with a modern sheen that is easy to clean. With stainless steel in particular, consistent maintenance is necessary to avoid a dulling of the backsplash’s shine.

Stone Slab

Sturdy? Check. Waterproof? Check. Classy? Check. From soapstone to marble to granite to good old-fashioned brick, there is no more low-maintenance backsplash base than stone. For the pleasure of acquiring a stone backsplash, you’ll typically pay more than most other materials. Between installation and material cost, the up-front payment can approach $1,000 for less than 30 square feet of wall space.

With a wide range of stone to choose from, a number of color options are available at varying costs. If that upfront payment is manageable, the results will blend both aesthetics and function, and stone’s resiliency makes any follow-up costs minimal.

For an expert DIY challenge, there are many other ways to create a satisfying backsplash that fits your fancy, including vinyl wallpaper, wood, and even beadboard. What’s your dream backsplash style?

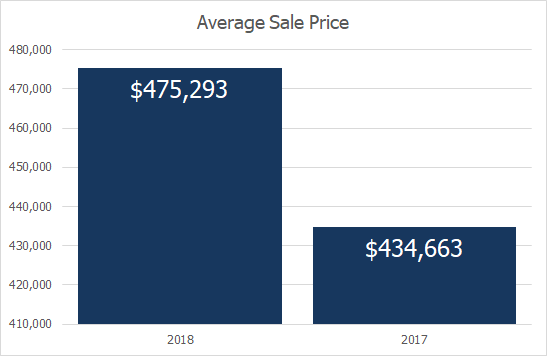

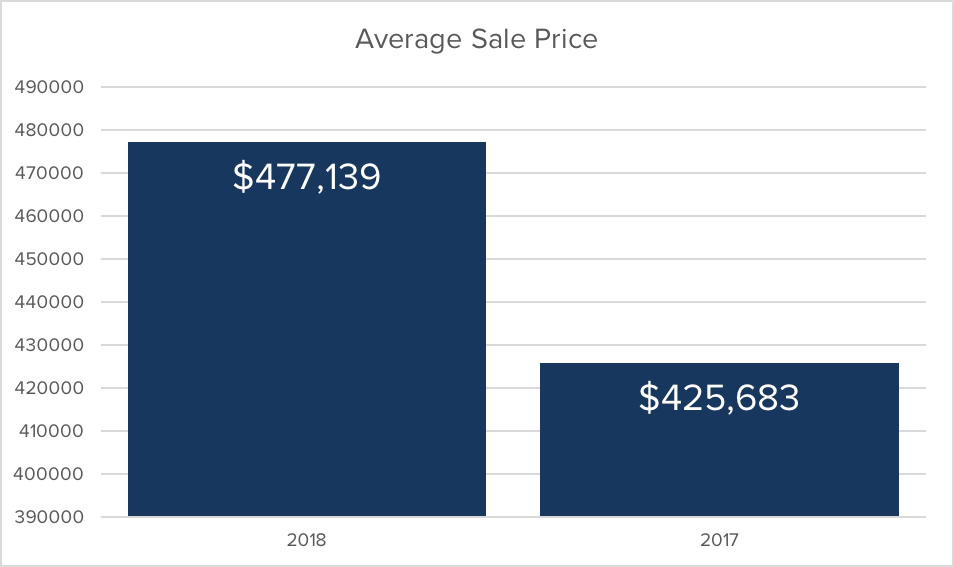

Local Market Stats For August

Marla Heagle, Windermere Stanwood Camano Island Owner

Every month, Windermere Stanwood-Camano publishes a snapshot of the local real estate market. Our Brokers use this data to help determine listing prices, realistic offers, and tailored advice for their clients. We also like to make this information public, to help you with your real estate journey. Here are our key takeaways from August 2018.

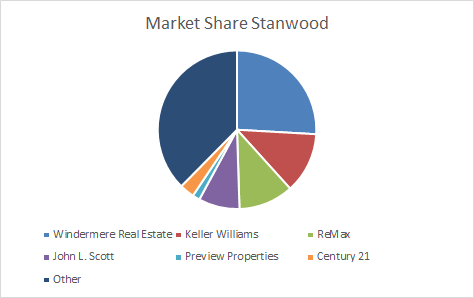

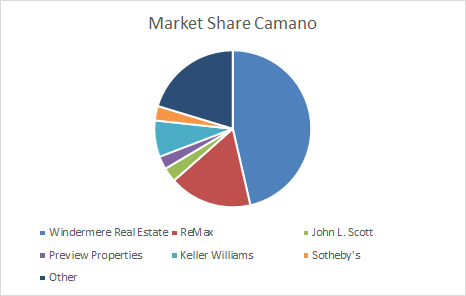

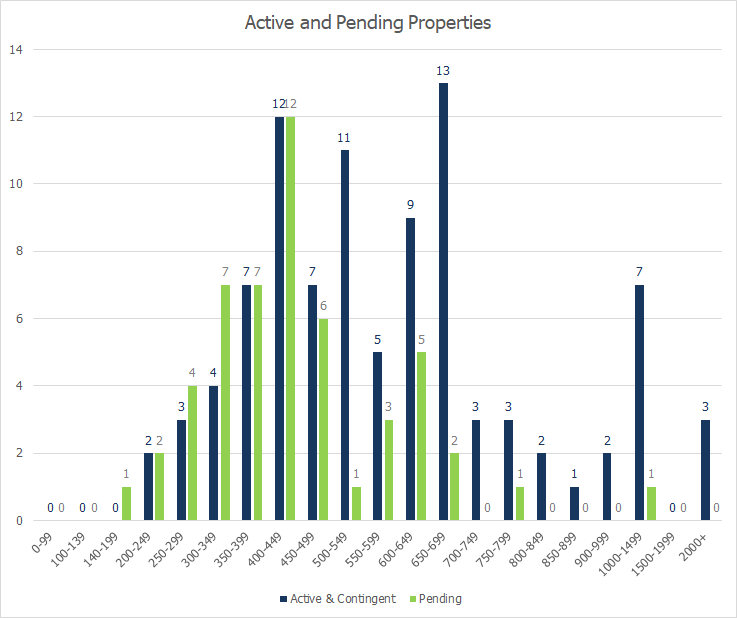

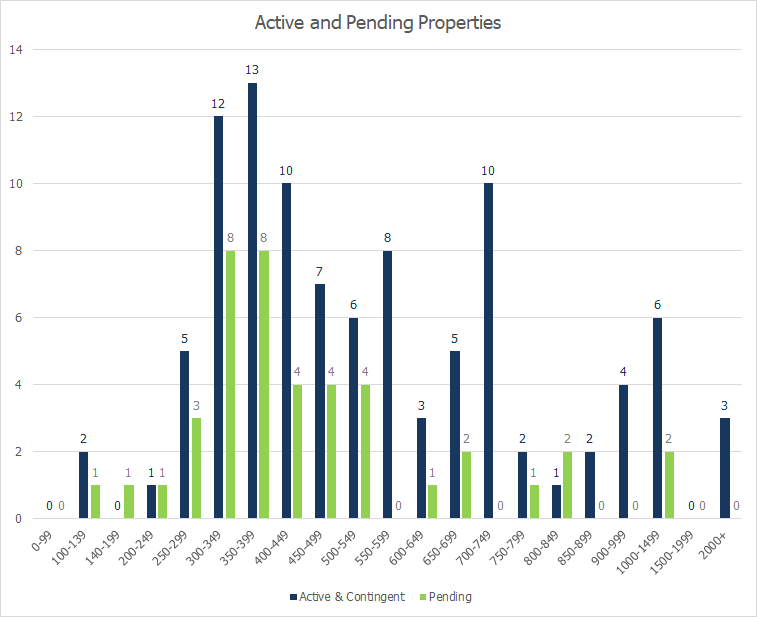

Stanwood & Camano Island

If you look at the pie charts below, Windermere has the largest market share with 26% of Stanwood and 46% of Camano Island. This means if you want to sell or buy a house in the area, we’ve got you covered with our talented, knowledgeable agents.

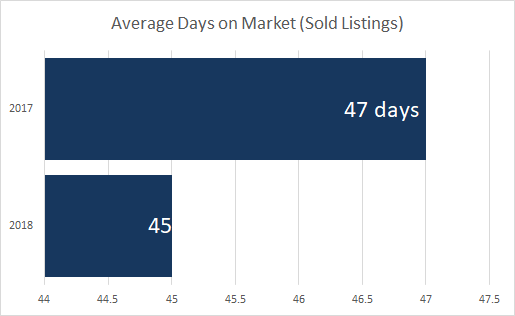

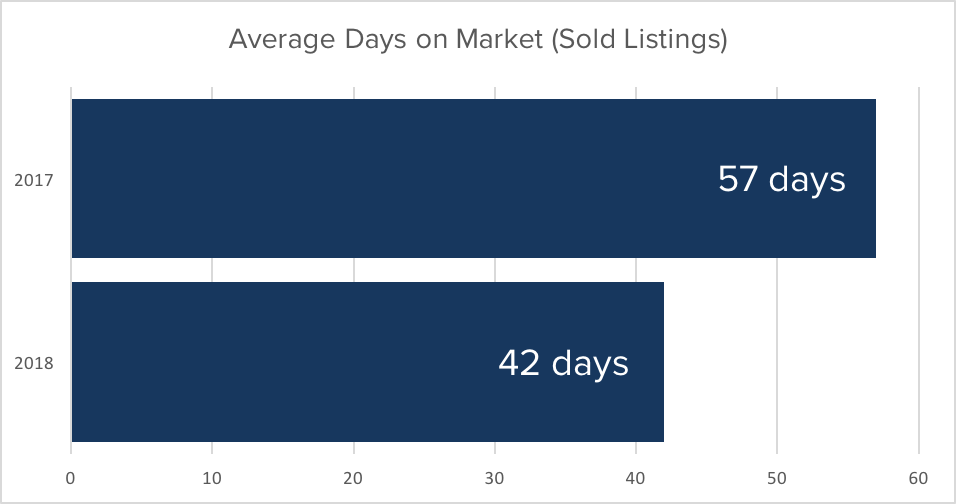

For Camano Island, the average number of days a home stays on the market is just 42, compared to 57 days last year. Last month, the average for Stanwood homes on the market dropped from 47 to 45 days, which is basically unchanged from the average in 2017 during the same months. Sellers can rest assured that in these particular areas, the fall season doesn’t have a negative effect on how fast a home sells.

Stanwood

Camano Island

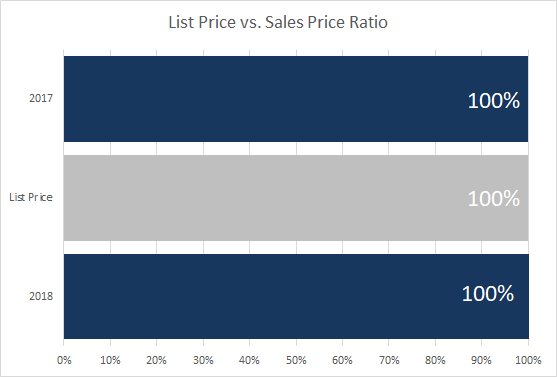

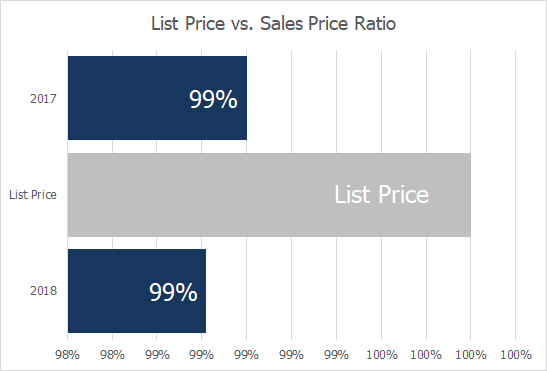

The average sale price of each home has increased dramatically over the past year–around $40,000 more per home for Stanwood and $50,000 more per home for Camano Island. This, of course, depends on a variety of factors and doesn’t necessarily mean your home’s value jumped that much, but the good news is that the list price compared to the sale price is just about 100% for Stanwood and Camano Island. This means there’s a good chance that if you price your home right to begin with (which we are experts at!) the price you ask for is likely what you’ll get offered.

Camano Island

Camano Island’s largest chunk of active and pending listings falls within the 350-399K price range. The highest number of homes sold within the last year falls within the same price range, too. If you think your home is valued 350-399K, it may be a good time to sell, as there is lots of activity in this price range.

Stanwood has a slight increase in this department, with the largest number of active listings in the 400-449K price range and pending transactions in the 650-699K price range. However, most homes sold in Stanwood this year fall within the 350-399K range, which is the same as Camano Island.

Stanwood

Camano Island

The bottom line is that if you’re interested in selling your home, don’t let the changing of the season deter you. Buyers will appreciate having more options and you’ll likely get the price you ask for. The good news for buyers is the market hasn’t gotten worse in terms of the number of listings and prices as summer has transitioned into fall.

View Full Stats – Stanwood

View Full Stats – Camano Island

Balancing a Home’s Personality and Amenities

It’s sometimes said that the limitations of a house are what help make it a home. For many, however, it is a point of pride to accept only the finest in their new residence. How can you find the balance between cultivating a lived-in home with personality and quirks versus a house with cutting-edge amenities that improve quality of life? To get to the bottom of that, we gathered a list six keys to consider when selecting and developing the home of your dreams:

The Neighborhood

Surprisingly, one of the biggest factors in choosing a new home isn’t the property itself, but rather the surrounding neighborhood. While new homes occasionally spring up in established communities, most are built in new developments. The settings are quite different, each with their own unique benefits.

Older neighborhoods often feature tree-lined streets; larger property lots; a wide array of architectural styles; easy walking access to mass transportation, restaurants and local shops; and more established relationships among neighbors.

New developments are better known for wider streets and quiet cul-de-sacs; controlled development; fewer aboveground utilities; more parks; and often newer public facilities (schools, libraries, pools, etc.). There are typically more children in newer communities, as well.

Consider your daily work commute, too. While not always true, older neighborhoods tend to be closer to major employment centers, mass transportation and multiple car routes (neighborhood arterials, highways and freeways).

Design and Layout

If you like Victorian, Craftsman or Cape Cod style homes, it used to be that you would have to buy an older home from the appropriate era. But with new-home builders now offering modern takes on those classic designs, that’s no longer the case. There are even modern log homes available.

Have you given much thought to your floor plans? If you have your heart set on a family room, an entertainment kitchen, a home office and walk-in closets, you’ll likely want to buy a newer home—or plan to do some heavy remodeling of an older home. Unless they’ve already been remodeled, most older homes feature more basic layouts.

If you have a specific home-décor style in mind, you’ll want to take that into consideration, as well. Professional designers say it’s best if the style and era of your furnishings match the style and era of your house. But if you are willing to adapt, then the options are wide open.

Materials and Craftsmanship

Homes built before material and labor costs spiked in the late 1950s have a reputation for higher-grade lumber and old-world craftsmanship (hardwood floors, old-growth timber supports, ornate siding, artistic molding, etc.).

However, newer homes have the benefit of modern materials and more advanced building codes (copper or polyurethane plumbing, better insulation, double-pane windows, modern electrical wiring, earthquake/ windstorm supports, etc.).

Current Condition

The condition of a home for sale is always a top consideration for any buyer. However, age is a factor here, as well. For example, if the exterior of a newer home needs repainting, it’s a relatively easy task to determine the cost. But if it’s a home built before the 1970s, you have to also consider the fact that the underlying paint is most likely lead0based, and that the wood siding may have rot or other structural issues that need to be addressed before it can be recoated.

On the flip side, the mechanicals in older homes (lights, heating systems, sump pump, etc.) tend to be better built and last longer.

Outdoor Space

One of the great things about older homes is that they usually come with mature trees and bushes already in place. Buyers of new homes may have to wait years for ornamental trees, fruit trees, roses, ferns, cacti and other long-term vegetation to fill in a yard, create shade, provide privacy, and develop into an inviting outdoor space. However, maybe you’re one of the many homeowners who prefer the wide-open, low-maintenance benefits of a lightly planted yard.

Car Considerations

Like it or not, most of us are extremely dependent on our cars for daily transportation. And here again, you’ll find a big difference between newer and older homes. Newer homes almost always feature ample off-street parking: usually a two-car garage and a wide driveway. An older home, depending on just how old it is, may not offer a garage—and if it does, there’s often only enough space for one car. For people who don’t feel comfortable leaving their car on the street, this alone can be a determining factor.

Finalizing Your Decision

While the differences between older and newer homes are striking, there’s certainly no right or wrong answer. It is a matter of personal taste, and what is available in your desired area. To quickly determine which direction your taste trends, use the information above to make a list of your most desired features, then categorize those according to the type of house in which they’re most likely to be found. The results can often be telling.

Local Law Enforcement Group Honors Heagles

![]()

Camano Law Enforcement Support Foundation last week awarded Randy and Marla Heagle with its inaugural Citizens of the Year award.

The Heagles have supported the group’s efforts for several years in a row, along with providing a space for the organization’s main annual fundraising event.

The foundation raises money to help Island County deputies and state park rangers by buying items such as a gun safe for the sheriff’s precinct, a speed radar trailer, trail cameras and money for the Shop with a Cop holiday program.

The award was presented by Foundation President Ram Prasad, who said that with help from people such as the Heagles, the group can continue helping people through efforts such as their “Be Safe, Be Visible” program.

For more information or to donate, visit clesfoundation.org or attend a regular meeting, held at 7 p.m. the first Monday each month at the Camano Country Club fire station.

Transforming Your House from a Summer Home to a Winter Hideaway

None of us want to admit it, but Winter is Coming. The new season of Game of Thrones might not be until 2019, but your home will need preparation before then. As the days shorten, you can mitigate many mid-winter headaches with some preemptive prep. Proper weatherizing can help protect your investment from preventable damage, save money on energy costs, and, most importantly, keep your home safe and warm for you and your loved ones throughout the winter season. Here is a useful checklist to manage your weatherization project. Setting aside some time on a couple Sundays should be more than enough to knock this out:

Getting started: Check your toolbox to make sure you have all the materials you need for home maintenance in one place. This NY Times article provides a good list of the tools you’ll really need to maintain your home. After your toolbox is put together, you can confidently begin the maintenance on your home.

Insulation: Insulating a home can reduce your energy bill by up to 50%. For the best results, your home should be properly insulated from the ceilings to the basement. By starting in your attic and progressively adding insulation to other areas of your home over time, you will avoid spending a large sum of money up-front.

Cracks & Leaks: Do a run-through of your entire house for cracks and leaks, from your roof to your baseboards. Winter weather is unpredictable. Whether your area gets rain, wind or snow, cracks in your house can lead to cold drafts or leaks that cause water damage. Depending on your house type, most cracks can be easily filled with supplies from your local hardware store in a do-it-yourself fashion. Use caulk to seal any cracks in the permanent building materials.

Windows & Doors: Another common place for heat leakage is in your windows and exterior doorways. Make sure seals are tight and no leaks exist. If you have storm windows, make sure you put them on before the cold season begins. Don’t underestimate the difference some weatherstrips and a door sweep can provide in preventing drafts and keeping the heat in.

Rain Gutters: Clean your rain gutters of any debris. In colder climates, buildup will cause gutters to freeze with ice, crack and then leak. Once you have removed the residue from the drains, test them by running hose water to make sure cracks and leaks have not already formed. Even in warmer locales, the buildup can put undue stress on your roof and home.

Pipes: Pipes are a number one risk in winter climates. A burst pipe can become a winter disaster in a matter of seconds. Remember to turn off your exterior water source and take in your hose. Internally, wrapping your pipes is a recommended precaution to take.

Heating System: What’s one thing gas fireplaces, wood burning stoves, and central air heating systems all have in common? They all need to be cleaned and maintained. Annual checks of are vital in avoiding dangers such as house fires. If you use an old-fashioned wood stove, make sure there are no leaks and that all soot build up or nests are removed. If a furnace is what you have, remember to change the filters as recommended or clean out your reusable filters.

Fireplace & Wood burning stoves: Make sure to have chimneys and air vents cleaned early in the season if you are planning on warming your home with a wood-burning source. When your fireplace is not in use make sure to close the damper, some resources estimate an open damper can increase energy consumption by as much as 30%.

Outside: As we mentioned before, make sure you bring your patio furniture inside (or cover) for the winter- but don’t forget other, smaller items such as your tools, including a hose and small planting pot. Clear out any piles around the side of your house, checking for cracks as you go so to avoid providing shelter for unwelcome guests over the cold season. If your property has large trees check for loose branches and call someone to trim back any items that may fall in your yard, on your roof or even damage a window.

Emergency Kit: Lastly, make sure your emergency kit is up-to-date with provisions, batteries, fresh water, food for animals, entertainment for kids, etc- especially if you live in an area prone to power outages.

How Reliable Are Home Valuation Tools?

What’s your home worth?

It seems like a simple question, but finding that answer is more complicated than it might seem. Sites like Zillow, Redfin, Eppraisal, and others have built-in home valuation tools that make it seem easy, but how accurate are they? And which one do you believe if you get three different answers? Online valuation tools have become a key part of the home buying and selling process, but they’ve been proven to be highly unreliable in certain instances. One thing that is for certain is that these valuation tools have reinforced that real estate agents are as vital to the process of pricing a home as they ever were – and maybe even more so now.

There are limitations to every online valuation tool. Most are readily acknowledged by their providers, such as Zillow’s “Zestimate”, which clearly states that it offers a median error rate of 4.5%, with varying accuracy across the country. That may not sound like a lot, but keep in mind that amounts to a difference of about $31,500 for a $700,000 home. For Redfin and Trulia, there are similar ranges in results. When you dig deeper into these valuation tools, it’s no small wonder that there are discrepancies, as they rely on a range of different sources for information, some more reliable than others.

Redfin’s tool pulls information directly from multiple listing services(MLSs) all over the country. Others negotiate limited data sharing deals with those same services, but also rely on public records, as well as homeowners’ records. This can lead to gaps in coverage. These tools can serve as helpful pieces of the puzzle when buying or selling a home, but the acknowledged error rate is a reminder of the dangers of relying too heavily on them.

Home valuation tools can be a useful starting point in the real estate process, but nothing compares to the level of detail and knowledge a professional real estate agent offers when pricing a home. An algorithm can’t possibly know about a home’s unique characteristics or those of the surrounding neighborhood. They also can’t answer your questions about what improvements you can make to get top dollar or how buyer behaviors are shaping the market. All of this – and more – can only be delivered by a trusted professional whose number one priority is getting you the best price in a time frame that meets your needs.

If you’re curious what your home might be worth, Windermere offers a tool that provides a series of evaluations about your property and the surrounding market. And once you’re ready, we’re happy to connect you with a Windermere agent who can clarify this information and perform a Comparative Market Analysis to get an even more accurate estimate of what your home could sell for in today’s market.

How to Acquire the Right Appraisal for Your Home

Appraisals are designed to protect buyers, sellers, and lending institutions. They provide a reliable, independent valuation of a tract of land and the structure on it, whether it’s a house or a skyscraper. Below, you will find information about the appraisal process, what goes into them, their benefits and some tips on how to help make an appraisal go smoothly and efficiently.

Appraised value vs. market value

The appraised value of a property is what the bank thinks it’s worth, and that amount is determined by a professional, third-party appraiser. The appraiser’s valuation is based on a combination of comparative market sales and inspection of the property.

Market value, on the other hand, is what a buyer is willing to pay for a home or what homes of comparable value are selling for. A home’s appraised value and its market value are typically not the same. In fact, sometimes the appraised value is very different. An appraisal provides you with an invaluable reality check.

If you are in the process of setting the price of your home, you can gain some peace-of-mind by consulting an independent appraiser. Show him comparative values for your neighborhood, relevant documents, and give him a tour of your home, just as you would show it to a prospective buyer.

What information goes into an appraisal?

Professional appraisers consult a range of information sources, including multiple listing services, county tax assessor records, county courthouse records, and appraisal data records, in addition to talking to local real estate professionals.

They also conduct an inspection. Typically an appraiser’s inspection focuses on:

- The condition of the property and home, inside and out

- The home’s layout and features

- Home updates

- Overall quality of construction

- Estimate of the home’s square footage (the gross living area “GLA”; garages and unfinished basements are estimated separately)

- Permanent fixtures (for example, in-ground pools, as opposed to above-ground pools)

After considering all such information, the appraiser arrives at three different dollar amounts – one for the value of the land, one for the value of the structure, and one for their combined value. In many cases, the land will be worth more than the structure.

One thing to bear in mind is that an appraisal is not a substitute for a home inspection. An appraiser does a cursory assessment of a house and property. For a more detailed inspection, consult with a home inspector and/or a specialist in the area of concern.

Who pays and how long does it take?

The buyer usually pays for the appraisal unless they have negotiated otherwise. Depending on the lender, the appraisal may be paid in advance or incorporated into the application fee; some are due on delivery and some are billed at closing. Typical costs range from $275-$600, but this can vary from region to region.

An inspection usually takes anywhere from 15 minutes to several hours, depending on the size and complexity of your property. In addition, the appraiser spends time pulling up county records for the values of the houses around you. A full report comes to your loan officer, a real estate agent or lender within about a week.

If you are the seller, you won’t get a copy of an appraisal ordered by a buyer. Under the Equal Credit Opportunity Act, however, the buyer has the right to get a copy of the appraisal, but they must request it. Typically the requested appraisal is provided at closing.

What if the appraisal is too low?

If your appraisal comes in too low it can be a problem. Usually, the seller’s and the buyer’s real estate agents respond by looking for recent and pending sales of comparable homes. Sometimes this can influence the appraisal. If the final appraisal is well below what you have agreed to pay, you can renegotiate the contract or cancel it.

Where do you find a qualified appraiser?

Your bank or lending institution will find and hire an appraiser; Federal regulatory guidelines do not allow borrowers to order and provide an appraisal to a bank for lending purposes. If you want an appraisal for your own personal reasons and not to secure a mortgage or buy a homeowner’s insurance policy, you can do the hiring yourself. You can contact your lending institution and they can recommend qualified appraisers and you can choose one yourself or you can call your local Windermere Real Estate agent and they can make a recommendation for you. Once you have the name of some appraisers you can verify their status on the Federal Appraisal Subcommittee website.

Tips for hassle-free appraisals:

- What can you do to make the appraisal process as smooth and efficient as possible? Make sure you provide your appraiser with the information he or she needs to get the job done. Get out your important documents and start checking off a list that includes the following:

- A brief explanation of why you’re getting an appraisal

- The date you’d like your appraisal to be completed

- A copy of your deed, survey, purchase agreement, or other papers that pertain to the property

- If you have a mortgage, your lender, the year you got your mortgage, the amount, the type of mortgage (FHA, VA, etc.), your interest rate, and any additional financing you have

- A copy of your current real estate tax bill, statement of special assessments, balance owing and on what (for example, sewer, water)

- Tell your appraiser if your property is listed for sale and if so, your asking price and listing agency

- Any personal property that is included

- If you’re selling an income-producing property, a breakdown of income and expenses for the last year or two and a copy of leases

- A copy of the original house plans and specifications

- A list of recent improvements and their costs

- Any other information you feel may be relevant

By doing your homework, compiling the information your appraiser needs, and providing it at the beginning of the process, you can minimize unnecessary phone calls and delays and get the information you need quickly and satisfactorily!

Here are a few Local Appraisers from Stanwood & Camano Island:

W.E. Kintner & Assoc. (360) 629-4216

PC Appraisal Company (360) 387-2043

Peterson Appraisal & Consulting (360) 629-0445

Hamilton Appraisal Services, Inc. (425) 422-3348

11 Ways to Uncover Your Personal Color Palette

Where do you find the colors you love? And just because you love a hue, does that mean it’s right for your walls? Let’s take a closer look at color inspiration. Here you’ll find tips for how to get your creative juices flowing and zero in on the color palettes that speak to you.

1. Be inspired by a landscape you love. Choosing your paint colors based on hues that occur together in nature takes some of the guesswork out of paint picking. The beach is the quintessential example of taking the landscape to a color scheme — the hues of sand, water and sky work beautifully as paint colors, as well as on furniture and accessories.

2. Snap pictures of colors that inspire you on walks and travels. Carry a camera and capture those little details that inspire you as you see them. Taking quick snapshots with your camera phone is fine — the point is more in the noticing than in the quality of your pictures. Sometimes the spirit of a place really shines through in the colors used there, so mine those old vacation photos for inspiration, too.

3. Notice the subtle hues that move you. Not everyone is drawn to bold, clear colors; that is only one small slice of the spectrum. Pay attention to the subtle hues and particular shades that move you, as these can become great color palettes. Perhaps you are drawn to the rich browns of worn leather and old wood. If you love blue, is it midnight, pale aqua or French blue? Get specific.

4. Try doing a color-a-day experiment. This practice is a workout for your creativity and visual sense. Look for shades of one color to photograph each day, until you have covered them all. Keep your eyes peeled for pretty veggies in the produce bins, graffiti on a brick wall, a row of colorful binders in your office — nowhere is off-limits.

5. Look to the branding of good restaurants, shops and other businesses. Shops are often great places for finding color schemes, since great care was taken to design them in an appealing way. The next time you walk into a shop or restaurant and find yourself really enjoying the atmosphere, stop and ask yourself why. Take a closer look at your surroundings — is it the paint color that makes you feel good? Try to begin naming what really works for you.

6. Pay attention to shop displays. When you’re inside a shop, pay special attention to beautiful displays of objects and flowers — especially color combinations that catch your eye. Notice which color was used in a larger swath and which color punctuates the arrangement. For instance, you may be drawn to a display of sunshine-yellow mugs, but upon further thought realize it’s the deep blue tile wall in the background that really makes it for you.

7. Consider the architecture of your home and the region you live in. What colors are typically used to play up the sort of house you have? Noticing doesn’t mean you have to follow suit, but it can help guide you in your process. Southwestern homes, for instance, tend to feature rich earth-tone colors, which complement the landscape beautifully.

8. Aim to complement what you already own. Look at what you already have in your home — do you tend to be drawn to bright, statement-y furniture with bold colors and patterns? If so, you may want to stick with neutral walls that won’t compete. If your furniture taste runs to white, white and more white, perhaps a subtle (but not white) neutral would add interest to your clean aesthetic. Assess the finishes in your home (floors, counters etc.) as well, since you can use them to find complementary wall colors.

9. Cast a wide net in what you read for inspiration. Decorating books are wonderful, of course, but also consider looking to graphic design, photography and garden books, and all sorts of magazines for inspiration. Save images that call out to you and begin a collection.

10. Experiment with inspiration boards. A board that works for another person may not work for you — so try out different methods until you hit on something that feels fun. Some may love the physical act of cutting and tacking up tear sheets to a board; others may find that fussy. Collect items in a tray or basket, create an ideabook on Houzz, slide your finds into a binder or stuff everything into a big folder.

11. Learn to translate what you see. Picking colors for your walls is a highly personal process. The best way to learn about what works for you is to start paying more attention to color … everywhere. Whether you are choosing colors on your own or working with a pro, this will hone your color sense and make picking paint a better experience all around.

The Risks and Rewards of Purchasing a Bank-Owned Home

The process of purchasing a home directly from a lender can be long and arduous, but could very well be worth it in the end. If you have your sights on a particular home or are looking to find a deal on your first, working directly with the lender may be your only option. Purchasing a bank-owned home is not for the faint of heart, here are some tips for negotiating the REO process:

1. Be prepared: The condition of bank-owned properties are often poor and hard to show. Past owners may have departed on bad terms, leaving the home in poor condition with foul smells, missing appliances, wires taken from breakers, gas fireplaces gone, even bathrooms without toilets and sinks.

2. Understand the costs: Maintenance or repairs may be necessary, since these homes have been vacant for an unknown period of time–sometimes months or years. Keep in mind, when they were occupied the owners could have been under a financial hardship, preventing them from doing regular seasonal care or repairs when needed. Remember as well that the bank is trying to sell the house immediately, so you will receive a financial break in the price rather than a willingness to negotiate on the maintenance and repair issues.

3. Accept the unknown: In traditional real estate transactions, homeowners fill out Form 17 regarding important information about the history of the house. A bank owned home is either exempt or marked with “I don’t know” throughout the document. Not having the accuracy of this 5-page disclosure form could leave you with a lot of unanswered questions on the history of the home.

4. Know what is non-negotiable: The pricing on the house may not get much lower. Some of these properties can be “a dream come true” if you get them at an amazing price, or they could be your worst nightmare. Do your due diligence researching any property, and conduct all necessary inspections to safeguard yourself. Some major repairs may be negotiable, but will likely not reduce the home price.

5. Make a clean offer: The higher the price you can offer, the better. Include your earnest money, keep contingencies to a minimum, and suggest a reasonable closing date. The simpler your offer is, the higher chance you have of the bank accepting your offer or countering in a reasonable time period.

6. Be patient: Consult with a professional who handles bank owned home purchases to help you negotiate the pathway to home ownership. The process of purchasing a bank-owned, foreclosed or short-sale home is typically longer than a typical real estate sale.